Beware of Unidentified Calls or Attempts to Gain Access to Your Online Banking Account

If you receive an unidentified call or voicemail about your online banking account, and you believe it to be suspicious or fraudulent, please hang up immediately and contact us at 800-475-1150. We are available to assist you.

Important Tips: Never provide your credit or debit card information, or online banking credentials to someone who calls you unsolicited. Be suspicious of any caller who asks for your personal information, such as your Social Security number or bank account number. If you are unsure about the legitimacy of a call, hang up and call us directly at 800-475-1150. We will never contact you to ask for your personal information or login credentials. A message from Collins Community Credit Union will always include identification.

A personal budget is a great tool to help you identify all of the income sources and monthly expenses you may have, and helps you see where you can cut back on your spending. Knowing exactly what your financial position is will help you make wise financial decisions in uncertain times.

Here are the simple steps to creating a personal budget worksheet:

Step 1: Identify your Income and Expenses

Before you can begin putting your budget together, you’ll need to identify all of the sources of income and expenses you have. Grab a piece of paper and a pen. On the front side of the paper, label it as Income and split the sheet of paper into 3 columns. Title the three columns “Source”, “Amount”, and “Frequency”.

Repeat this step on the back of the paper, but label it as Expenses.

- Identify your income: For most people, this is the easiest part of the budget. It’s important to know how much income you have as well as your different income sources (for example, paychecks, social security, tax refunds, child support, etc.). Do not write down any possible income at this time. Possible income includes bonuses, a one-time asset sale (home or car sale), or cash rewards based on spending.

- Identify your expenses: A good way to identify all of your common monthly expenses is to review the last two months of your bank statements and credit card purchases. Common expenses include your mortgage/rent, cable, heating/cooling, child care, your phone bill, and groceries.

Step 2: Identify Monthly Net Income/Loss

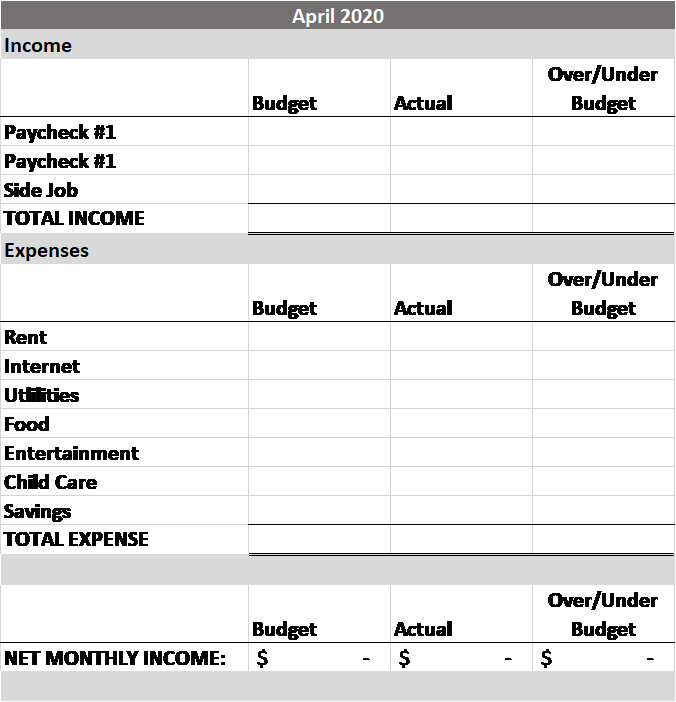

Once you have your income and expenses written down, it’s time to place them into a budget worksheet. There are many versions of budget worksheets that can be found online. A budget worksheet should look similar to this:

Your net monthly income will be the result of taking your total income minus your total expenses.

Step 3: Make Necessary Adjustments To Create a Positive Income

This step is the key reason for having a budget! A budget is set so you know how to live within the income you receive. If you completed steps one and two and had a negative balance for your total monthly income, then you need to look at ways to cut your adjustable expenses. Adjustable expenses are variable and can include dining out, entertainment, groceries, home or auto insurance (Reach out to the Collins Insurance team for a free quote and to discuss different options that might save you money!), and your cable, phone, and internet service.

Step 4: Enter Monthly Expenses

Now that you’ve mapped out your budget it’s time to test it! Track all of your spending on your budget worksheet at least twice during the month. You will be over budget if your actual expenses for the current month ended up being more then your budgeted expenses. Reviewing this will give you a snapshot in time of what your current financial position is.

Step 5: Control Over Budget Expenses:

If you’re over budget by month-end, then review the areas where you went over, and ask yourself the following questions: Did I need everything that I purchased? Could I have purchased less? Could I find ways to decrease the amount spent next month? If you can’t cut back on expenses, then start looking into ways to increase your monthly income.

Step 6: Be Patient and Stick with the Budget Process:

Be patient with your budget. It may take multiple months of tracking and adjusting to get a budget that works with your finances and lifestyle. Keep in mind that the overall goal of a budget is for you to live within the income that you generate. If you stay diligent at tracking your monthly income and expenses, you’ll find a financial balance in your life.